New public offers and admissions to trading regime: FCA publishes further details - Highlights for Equity Capital Markets

Protection for certain forward-looking statements

To encourage issuers to disclose in prospectuses (especially IPO prospectuses) more detailed forward-looking information, particularly in relation to expected future financial performance and sustainability objectives, the POAT Regulations establish a different liability threshold, based on fraud or recklessness, for certain categories of forward-looking statements that meet certain criteria. These will be known as “protected forward-looking statements” (PFLS).

The FCA is empowered to specify which types of statements should qualify as PFLS and the labelling and other requirements that should apply to them. It proposes that most mandatory disclosures required by the Annexes will not qualify as PFLS. But any profit forecast, and certain information that must be included in the Business Overview (including certain climate-related items (see above)), Operating and Financial Review and Trend Information sections will qualify as PFLS if the information satisfies the relevant criteria. The proposed criteria, which are based on the requirements that apply to profit forecasts, and on US practice, are very specific: unless they are widened, many forward-looking statements are unlikely to qualify. Profit estimates, aspirational targets and most purely narrative statements will not qualify as PFLS.

All PFLS disclosures will need to be clearly labelled, and certain accompanying statements will have to be included.

The higher threshold for liability applies only in respect of statutory liability to pay compensation to investors under Regulation 30 of the POAT Regulations (which will broadly replace section 90 of the Financial Services and Markets Act 2000). Where the prospectus relates to a transaction with a US or other overseas element, if the issuer intends to include forward-looking statements, it will also to consider the risks of liability under relevant overseas laws and how they can be mitigated.

Supplementary prospectus and withdrawal rights

Existing rules around when a supplementary prospectus must be published and withdrawal rights can be exercised will be retained broadly as they are.

"Six-day" rule on IPOs with a retail offer

As recommended by the SCRR, the existing requirement that, in the case of an IPO involving an offer to the public, the prospectus must be published at least six working days before the end of the offer, will be amended to reduce the period to three working days. This is designed to encourage issuers to include a retail offer in their IPO.

Admission of securities to a primary MTF

An “MTF admission prospectus” will usually be required where (i) an issuer seeks initial admission to trading on a primary MTF on which retail investors can trade, even if there is no fundraising; or (ii) an enlarged entity seeks re-admission to such an MTF following a reverse takeover. An MTF admission prospectus will be subject to the same statutory responsibility and compensation provisions, and the same PFLS rules, as apply to prospectuses.

However, operators of primary MTFs will have discretion to decide (i) whether an MTF admission prospectus will be required for a secondary fundraising; (ii) the information that must be included in an MTF admission prospectus; and (iii) the process for reviewing and approving an MTF admission prospectus.

By introducing the concept of an MTF admission prospectus, the Government is hoping to encourage primary MTF issuers to offer securities to retail investors, instead of limiting their offer to qualified investors or fewer than 150 persons.

PUBLIC OFFER PLATFORMS: CP 24/13

Operating a public offer platform will be a regulated activity, so a firm wishing to operate one will need to apply to vary its existing permissions or seek authorisation from the FCA. According to the FCA, there are currently 27 crowdfunding platforms operating in the UK: some of these are likely to apply for permission to operate a public offer platform. Other firms may also apply.

Shares offered via a public offer platform will almost certainly be riskier than shares bought on a public market: platform operators will therefore have a key gatekeeping role in deciding if a public offer should be made to investors. To address potential information asymmetry and guard against potential fraud, a new Chapter 23 of the FCA’s Conduct of Business sourcebook (COBS) will specify:

- The information-gathering and due diligence that platform operators should carry out on prospective issuers and the securities being offered. Among other things, before facilitating a public offer, a platform operator will have to:

- obtain certain minimum information on the issuer, including its directors and senior management, persons capable of exercising significant influence over it, the issuer’s group, its business model, intangible assets, risk factors, litigation, material contracts, historical financial information, financing structure and creditworthiness;

- obtain certain information about the securities to be offered, how the proceeds will be used and any materials that will be used to market the offer;

- carry out a reasonable verification exercise on the information collected. Factual information will have to be verified by reference to reliable sources; non-factual information will be subject to a “plausibility assessment”;

- carry out a reasonable assessment of the issuer’s creditworthiness; and

- assess whether the issuer and its securities are appropriate to be offered to the public.

- The information a platform operator must provide to investors. This will include:

- a “disclosure summary”, in a prescribed format, of the issuer and the public offer, including (i) a summary of the information provided by the issuer and verified by the platform operator; (ii) a description of the checks and verification undertaken by the operator, including in relation to the plausibility of non-factual information and the creditworthiness assessment; and (iii) the operator’s assessment of whether it is appropriate to facilitate the offer. Proprietary or commercially-sensitive information will not have to be included;

- the most recent financial statements of the issuer, including whether they have been audited;

- the terms and conditions, and other contractual documents; and

- any other information needed for investors to make an informed decision whether to participate in the offer.

While the offer remains open to the public, the above information will have to be available to platform investors and the operator will have to make available in real time the amount raised by the issuer via the offer. The FCA seeks views on whether operators should be required to disclose updated information after an offer has closed.

- How legal liability and redress will apply to platform operators and issuers. If an operator falls short of the standards imposed by the FCA, an investor may have a private right of action under section 138D of the Financial Services and Markets Act 2000 and the operator may need to compensate the investor’s loss. No special liability regime will be imposed on issuers, but investors may be able to use common law remedies to seek compensation from an issuer in case of insufficient, false, or misleading disclosures. An issuer could also be liable to the platform operator for breach of its terms and conditions if it fails to disclose all relevant information.

If a firm wishes to offer ‘secondary trading’ type facilities as well, it will need appropriate FCA permissions for this. One option would be to provide secondary trading under the proposed new Private Intermittent Securities and Capital Exchange Systems (PISCES) regime, which initially will operate via a regulatory sandbox. (Further details of the PISCES regime will be included in a briefing to be published shortly.)

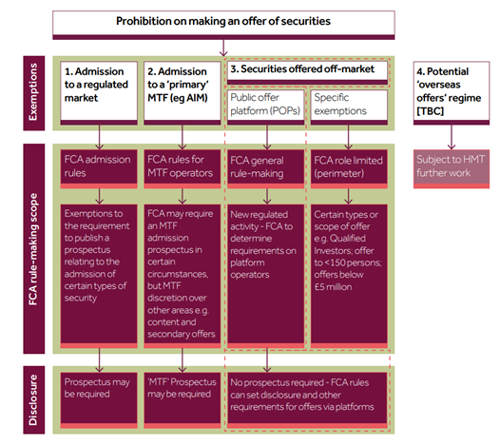

NEW PUBLIC OFFERS REGIME: DIAGRAMMATIC SUMMARY